Steady 2026 Spending Reflects Continued Normalization

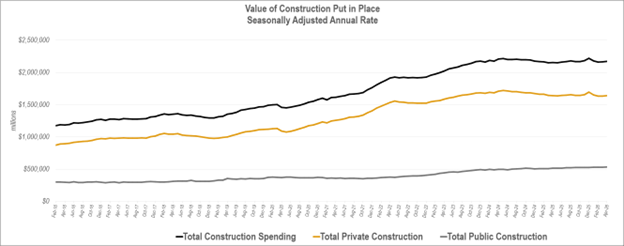

Recently, the U.S. Census Bureau released its latest Value of Construction Put in Place survey, which provides monthly estimates of the total dollar value of design and construction work completed across public and private projects. According to the April 2026 results, total spending continued to stabilize, reaching a seasonally adjusted annual rate of $2.17 trillion—a modest increase from March (+0.4%) and slightly above the level recorded one year earlier (+0.9%). The overall trend remains steady and consistent, supported by broader economic conditions that have held relatively stable.

Public and private spending patterns reinforce this stability. Private construction reached $1.64 trillion in April (+0.4%), continuing to represent the majority of total activity. Public construction totaled $532.73 billion, also slightly higher (+0.4%) than the previous month. Year-to-date data shows that public spending remains a reliable market, backed by multi-year federal and state infrastructure programs. Together, these dynamics reflect the gradual normalization engineering firms have experienced over the past year.

Source: US Census Value of Construction Put in Place Survey June 1, 2026, release

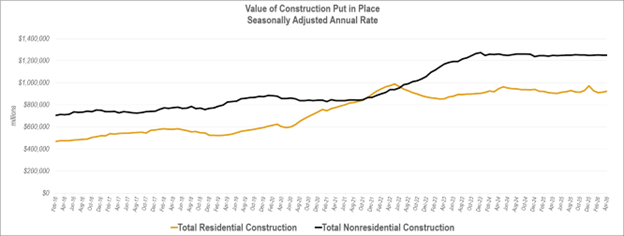

Residential construction reached a seasonally adjusted annual rate of $922.04 billion in April, reflecting a small monthly increase (+0.8%). The category continues to benefit from limited housing supply, steady multifamily development, and an active renovation market. Despite renewed rate pressures tied to the Iran conflict, residential activity has remained relatively consistent, supported by underlying demand drivers. Together, these conditions continue to sustain demand for land development, building design, and permitting services.

EXPLORE THE DATA WITH OUR INTERACTIVE DASHBOARD

Nonresidential construction totaled a seasonally adjusted annual rate of $1.25 trillion, which is essentially unchanged from March (+0.1%). Within this category, year-to-date data shows steady activity across several key markets. Office construction is posting solid year-to-date growth, supported by data center development. Commercial construction is also modestly higher than a year ago. Manufacturing, healthcare, and power-related construction continue to provide reliable opportunities for engineering firms as investment in industrial capacity, medical facilities, and energy infrastructure remains active.

Despite declines in the manufacturing sector, it remains the largest market by dollar value, and activity has remained consistent.

Source: US Census Value of Construction Put in Place Survey June 1, 2026, release

Current spending patterns highlight several forces shaping the landscape. Federal infrastructure funding continues to support a predictable pipeline of civil and transportation projects. Housing demand remains strong enough to sustain residential activity even in a higher-rate environment. Manufacturing spending remains historically high, with monthly variations tied to the timing of large project phases. Firms with strong capabilities in transportation, water, environmental, industrial, and multifamily work will be well positioned for the remainder of 2026.