New Data Signals Shift from Manufacturing to Digital Infrastructure

Recently, the U.S. Census Bureau released its latest Value of Construction Put in Place (CPiP) survey, which provides monthly design and construction spending for public and private sectors. With the May 2026 release, the U.S. Census Bureau revised unadjusted data back to January 2024 and seasonally adjusted data back to January 2019, altering historical benchmarking.

The revised data shows that the market entered 2026 unevenly, with overall spending essentially flat and momentum varying by sector. The manufacturing-led boom that drove growth in recent years is moderating, while investment tied to office, power, communications, and data center-related infrastructure is emerging as the next major source of activity.

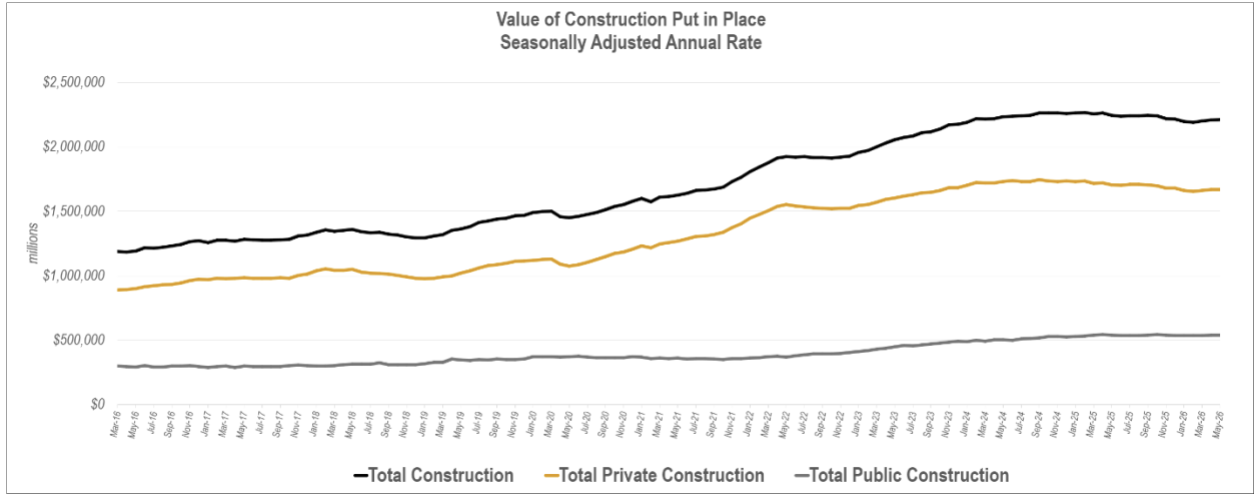

According to the May 2026 release, total spending reached a seasonally adjusted annual rate (SAAR) of $2.21 trillion, up 0.1% from April but down 1.5% from May 2025. Private construction totaled $1.67 trillion, essentially unchanged month over month and down 2.1% year-over-year, while public spending increased 0.5% from April and remains slightly above last year. While private investment continues to cool, public spending remains a stabilizing force for the overall market.

EXPLORE THE DATA WITH OUR INTERACTIVE DASHBOARD

Source: US Census Value of Construction Put in Place Survey July 1, 2026, release

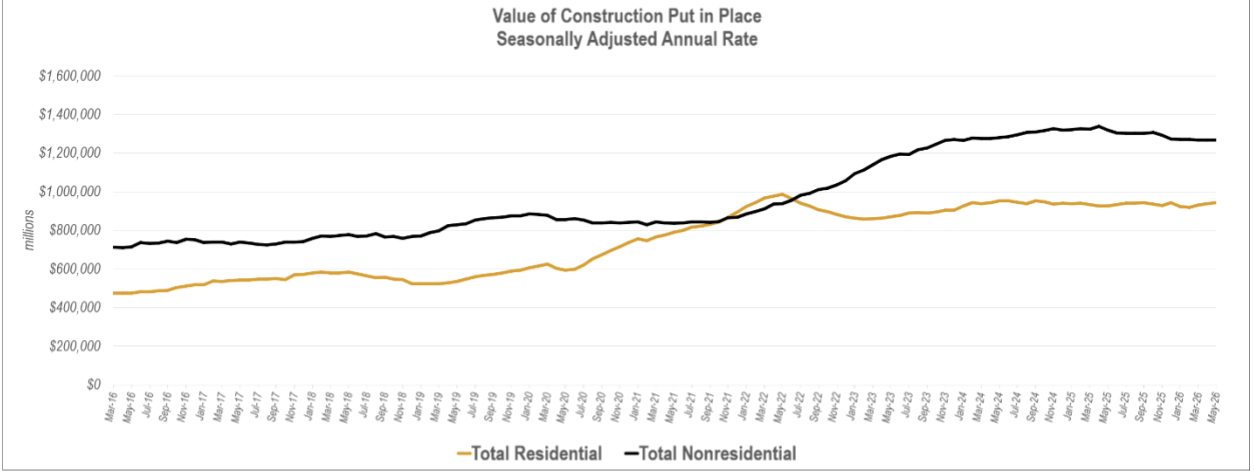

Residential spending reached $942.8 billion SAAR in May, up 1.8% year over year, reflecting continued demand despite elevated mortgage rates and ongoing affordability challenges. Nonresidential spending totaled $1.27 trillion SAAR, down 3.8% year over year, reflecting weakness across large market sectors. Much of that decline can be traced to weaker manufacturing activity, which has cooled after several years of investment.

Source: US Census Value of Construction Put in Place Survey July 1, 2026, release

Manufacturing remains the largest nonresidential market, but year-to-date spending through May declined 22.4% compared to 2025. Commercial, lodging, educational, and public safety markets also posted declines. While some of this weakness reflects the recent revision by the U.S. Census, it also suggests the market is moving beyond the peak of the recent industrial construction cycle.

At the same time, Religous, Conservation and Development, Amusement and Recreation, Office, Communications, and Power all posted year-to-date growth. Office, Power, and Communications are particularly notable because they capture or support investment in data centers, cloud computing, grid modernization, and other assets supporting the digital economy.

Taken together, the data suggest construction activity is becoming increasingly bifurcated. Traditional growth drivers tied to manufacturing expansion are moderating, while office, power, communications, and digital infrastructure are emerging as the next generation of project investment.