The Cost of Conflict: Mideast Tumult Hits Oil Prices, Pinches Supply Chain

Oil prices are grabbing headlines and dominating boardroom discussions for good reason. But upon digging into the data, it’s the impact of supply chain congestion that will have a longer-term effect on costs for construction projects, affecting engineering & design firms’ bottom line.

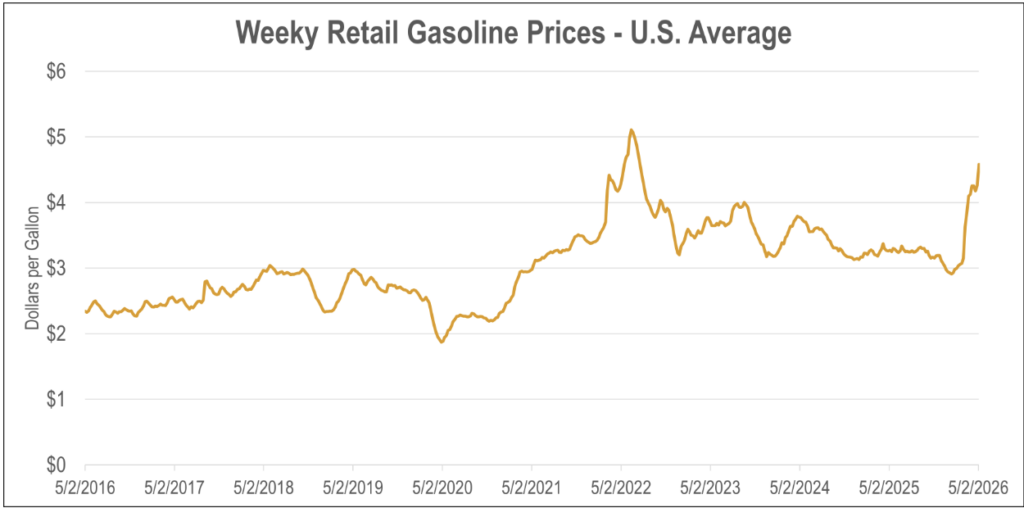

As of this writing, there is still no permanent resolution to the conflict in the Middle East or the concurrent rise in the price of oil, which has dealt a body blow to the U.S. economy. These spikes in oil prices pass through to the pump, where households now pay $4.58 a gallon as of May 4, compared to $3.08 on February 23—a 49% increase in less than 3 months.

Source: U.S. Energy Information Administration, Weekly Retail Gasoline and Diesel Prices

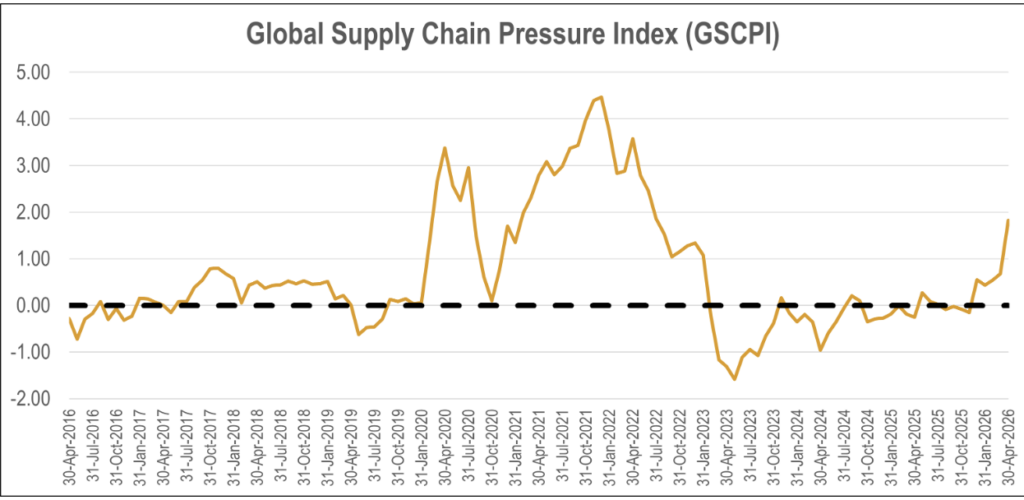

An equally consequential impact will be the supply chain disruptions caused by the Strait of Hormuz congestion. The most recent measure of the Global Supply Chain Pressure Index from the Federal Reserve Bank of New York at the end of April was 1.82. The last time the GSCPI was this high was July 2022.

Source: Federal Reserve Bank of New York

For the architecture, engineering, and construction industry, the key question is how these developments will affect project costs.

Our analysis finds that:

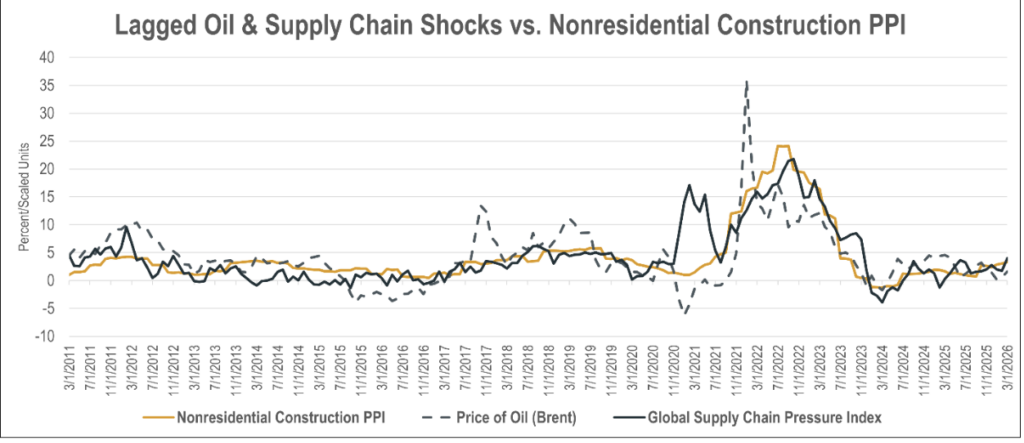

- These shocks have their strongest impact on costs 8 to 9 months after they first happen;

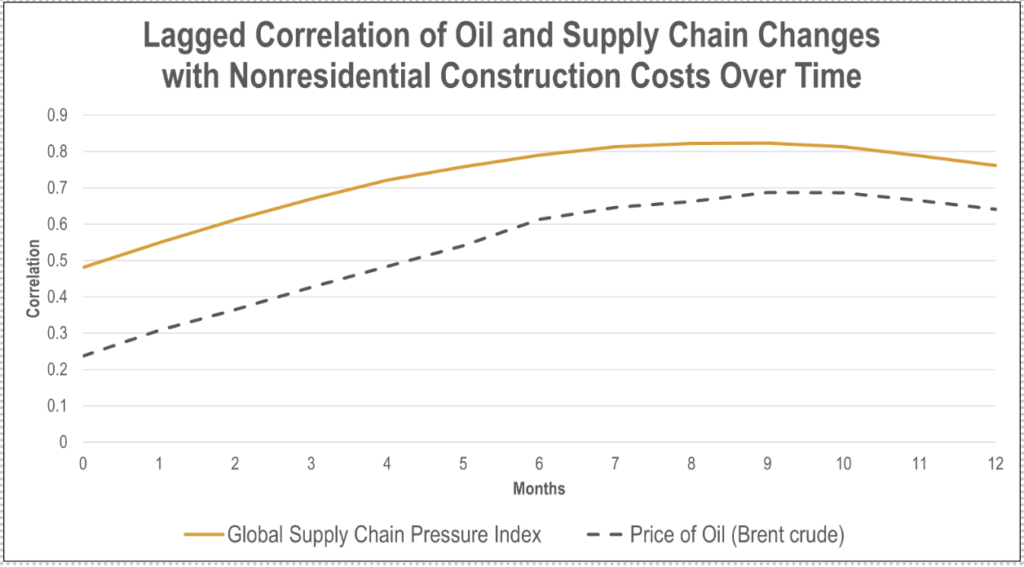

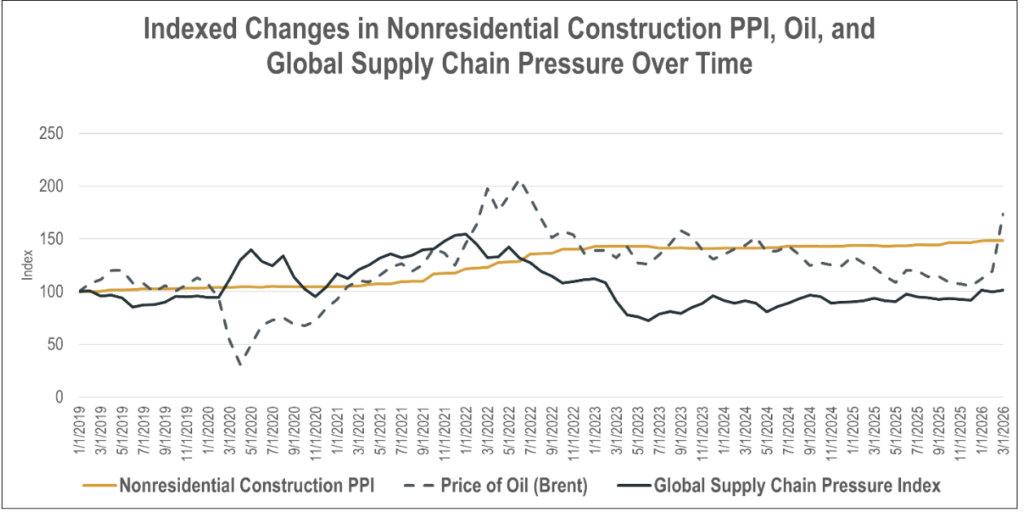

- While oil has a relationship with nonresidential construction costs, supply-chain pressure shows the stronger and more pronounced relationship in the data;

- Construction costs are extremely “sticky.” Once they increase, they rarely decrease, even if there are decreases in oil and supply chain pressure.

Source: U.S. Bureau of Labor Statistics, U.S. Energy Information Administration, Federal Reserve Bank of New York, ACEC Chief Economist Analysis

Why this matters for AEC firms

For AEC firms, the practical lesson is not to stop watching oil price movements, but, to consider that for project cost impacts supply-chain stress is a broader measure.

It can reflect disruptions related to logistics, delivery times, production bottlenecks, shortages, and shipping friction across multiple categories of inputs. That broader reach may help explain why its relationship with nonresidential construction PPI appears stronger than oil’s impact.

It is crucial to track supply-chain pressure alongside oil, and to give attention to the supply-chain signal when planning for future cost changes, particularly for firms deciding:

- Project budgeting

- Procurement timing

- Escalation clauses

- Owner communications

- Risk monitoring

Source: U.S. Bureau of Labor Statistics, U.S. Energy Information Administration, Federal Reserve Bank of New York, ACEC Chief Economist Analysis

How We Came to This Conclusion

To test which factor has the stronger relationship with construction costs, we estimated a lagged regression model using monthly data on nonresidential construction producer prices, Brent crude oil prices, and the Global Supply Chain Pressure Index. This approach accounts for the fact that cost shocks do not hit construction projects all at once; they tend to flow through bids, procurement, materials, and contractor pricing over several months.

The results point to an 8- to 9-month delay. A one-unit increase in the GSCPI is associated with roughly a 0.26% increase in nonresidential construction producer prices after nine months. A 10-percentage-point increase in Brent oil price growth, by contrast, is associated with only about a 0.02% increase after eight months and is not statistically significant in our current independent variable analysis.

For visual comparison only, we’ve plotted the timing and shape of change to the data overtime below.

Source: U.S. Bureau of Labor Statistics, U.S. Energy Information Administration, Federal Reserve Bank of New York, ACEC Chief Economist Analysis

In short, oil prices are a visible cost pressure, but supply-chain stress is the more important warning signal for nonresidential construction costs.